ECA asked Ross Caveille of Acorn-I to look at the data around Black Friday sales on Amazon and give us the headlines around what really happened

We analysed more than 62,000 products sold by 100’s of brands during Black Friday week to gain an understanding of shopper behaviour during this period. Predominantly, the markets we analysed were US and UK. Year on year analysis is comparing Black Friday period 2020 and 2021.

Summary of key items of interest:

- Direct-To-Consumer (DTC) delivered the greatest percentage uplift of sales YoY, on average +33%, vs Amazon which delivered just over +4%.

- Average basket size of DTC websites was +155% greater than the average basket size on Amazon.

- Amazon delivered strong New-To-Brand (NTB) sales. Of total sales on Amazon, 61% were from new customers that had not previously purchased from the brand.

- NTB customer revenues on Amazon grew by +49% YoY.

- Via DTC channels, existing customers accounted for 51% of total sales, an increase of +39% YoY.

- Advertising is more competitive, sponsored listings cost-per-click up +42% YoY.

- Sales for consumer goods, including grocery and snacks categories, were all down YoY.

- Homecare and personal care-related categories were the winners in terms of YoY revenue growth.

Black Friday / Cyber Monday Week

Shopping events such as Black Friday, Cyber Monday and Prime Day are key periods for many companies due to the significant increase in Sales to both new and existing customers. This year proved no different albeit the dynamic between Amazon and DTC channels is changing.

Leveraging Acorn-i’s proprietary software we saw that total omnichannel sales across all measured markets over the course of this last week resulted in a +16.8% increase compared to the same period in the previous year.

The increase was driven by a blend of both Existing Buyers, 40.9% of sales generated by existing customers, and New Buyers, 54% of sales generated by previous purchasers.

The total sales value of NTB customers was >22% higher than the same period last year. This was driven primarily by an increase in the number of absolute new buyers as well as the number of orders placed per buyer which grew >2%.

Existing and returning customer sales increased +70% vs the same period in 2020. This was driven by a combination of; the number of buyers which grew +55%, the number of orders per customer +50%, as well as the average order value which increased +14%.

Digital Retail Channel Mix

While most brands experienced an increase in sales via Amazon, the greater percentage sales lift YoY was from D2C channels. The evolution of platforms such as Shopify over recent years has made it simpler for brands to develop eCommerce functionality. DTC sales grew +33.6% during Black Friday week vs the same period in 2020.

There is a clear dynamic forming between Amazon and DTC channels. Revenues from NTB customers on Amazon represented 61% of total experiencing solid YoY growth of +49%. Just over half of DTC revenues were generated by repeat customers with the value of NTB purchasers increasing by +12.5% YoY.

It’s increasingly important for brands to understand how consumers find, engage with and purchase their products cross-channel. Brands need to develop mechanisms to measure channel impact according to the value proposition of the channel – if one channel drives predominantly NTB arguably this allows for high customer acquisition cost vs driving repeat purchase.

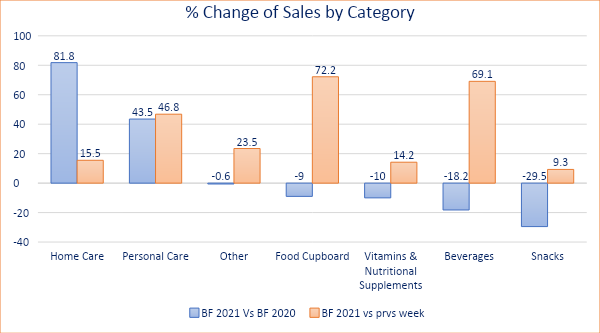

Category Winners/Losers

Homecare, Personal Care, Consumer Electronics and Baby care categories all saw YoY growth in comparison to Black Friday period 2020. Purchasing intent and sales specifically for home and personal care related items performed above average category growth benchmarks.

Categories within Grocery / Food Cupboard, such as coffee, condiments, snacks and meal kits, experienced on average a decline in sales compared to the same period in 2020. The softness in sales growth YoY likely due to societal impacts due to 2020 lockdown vs broader channel shopper choice in 2021.

All categories and brands enjoyed week-on-week sales lifts. Black Friday proved again to be an event that it’s better to include within your sales and promotions strategy than not when looking to acquire new and upsell to existing customers.

Advertising Costs Increase

Being ‘top-of-search’ on page one on Amazon search results is the optimum placement to capture shopper intent and drive higher Return On Advertising Spend (ROAS). Year on year Amazon has increased the volume of sponsored placements across its website and competition has intensified.

Amazon is increasingly ‘pay-to-play’ but Black Friday week saw competition across all digital channels:

- Amazon Sponsored Products CPC increased by +23% WoW.

- Amazon Sponsored Display CPC increased +109% WoW.

- Amazon Sponsored Brands CPC increased +30% WoW.

- Facebook, driving to Amazon or DTC sites, CPC’s increased +81% WoW.

- Google search ads CPC decreased by -2% WoW.

Brands can win in ever more competitive environments by using differentiated tactics, some of which as follows:

- Leverage Amazon shopper search data to inform manual targeting lists.

- Apply top clicked and purchased product ASINs to product targeting campaigns to drive scale and sales volumes.

- Maximise reach of Sponsored Brands Video, a uniquely CPC video solution.

- Optimise cross-channel campaigns via a single solution to maximise investment value.

- Leverage Amazon Attribution to measure effectiveness of off and on Amazon campaigns via consistent metrics.

- Amazon DSP custom audiences can provide a powerful targeting segment to reach engaged shoppers that have yet to purchase.

- Leverage technology solutions to optimize Amazon Advertising campaigns using Amazon retail data.

- Apply machine learning technologies to automate >1,000’s of search terms, placements, bids variations.